Good Morning,

Good Morning,

Thursday’s improvement in risk appetite brought gold values to near the bottom of their current $1,240-$1,265 range. However, the relatively small decline from near-record levels was partially countervailed by overnight gains in the yellow metal attributable to some bargain hunting and continuing perceptions that not all is well with the state of global economics.

PR outlets were quickly tasked with heavily disseminating the-thought-to-be-market-supportive news that Bangladesh agreed to take 321,510.00 ounces of bullion off the IMF’s hands, in a rebalancing move that places it from 77th to about 58th on the list of top 100 gold holders in the world. Its previous 3.5 tonne holding was neck-in-neck with…Canada’s official gold stash.

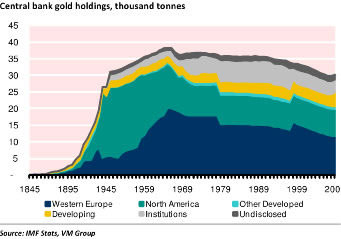

As for the IMF, this small, direct-to-the-official-sector sale does not preclude continuing sales of its leftover gold via market channels, in a similar manner in which it has already disposed of about 88 tonnes of its original 403 ‘must-sell’ tonnage. At previous ‘burn’ rates, such disposals could be completed by late 2010/ early 2011. And, in case you are wondering what this entire process involving central banks’ new putative love affair with gold looks like in graphical terms, here it is:

It is but a process; an ever-changing one that involves — as has often been posited here-no more than individual allocation policies and decisions made on what is ‘adequate’ in terms of holding in gold. The only consistency in central bank gold policies appears to be one of inconsistency. In reality, there’s neither an "ideal" gold holding level, nor any predictable uniformity in allocation policy among various central banks.

Why does Portugal have 83.8% of its reserves in gold? Maybe it’s Columbus’ legacy. Why does China feel that 1.5%-2% is ‘sufficient’ to keep in gold? Maybe Confucius rubbed off on someone:

"The scholar does not consider gold and jade to be precious treasures, but loyalty and good faith."

Answers as good as any. Why does the US value its 8,100+ tonnes at $42.20 an ounce? Why does Canada feel safe with practically no gold in its basement? Questions as good as any. But, you get the point; don’t try to guess.

No specific central bank (except for Saudi Arabia and South Africa) keeps the exact ‘world average’ of about 10% in gold holdings (a figure which this writer recommends for your own ‘reserves’ by the way). The fact is that most countries have either a lot lower or a lot higher holdings in the yellow metal. Internal policy comes first, not the wishes of hard-money newsletter writers, or the assumptions being made by recent investors in gold based upon reading said newsletters.

The final trading session of the week started out on a promising note for gold, but the action soon turned to selling (within the first ten minutes of market action) despite the Bangladeshi purchase. Whether the combination of pre-weekend book-squaring and the slight lift in the US dollar will continue to push prices lower on the day remains to be seen.

Early on Friday, the complex was in the red for all but silver values at last check. Indications harvested during said check: gold spot bid at $1,235.70, silver spot bid at $19.90, platinum spot bid at $1545.00 and palladium spot bid at $519.00 per ounce. Another day at $2,080.00 for rhodium. However, the tone shifted later in the morning and gold drew closer to $1,250 while silver overcame the $20.00 mark once again (or, perhaps, it kinda dragged gold higher in its wake).

On other fronts, the world news flows continued to yield a mixed bag of reports; some good, some not-so-hot. Take the wacky Florida pastor’s decision to place the burning of a certain holy text ‘on hold’ — file under ‘good news.’ Sadly, at least one person has been reported killed already as a result of that man’s idiocy. Then take Jean-Claude Trichet’s assertion that the ‘special credit support’ (now there‘s a new label to start using for crisis reportage!) may take a while to ‘phase out.’ File that one under ‘speaking clearly not.’ Mr. T gave no timelines for the exit to take place. File that one under ‘that’s no surprise.’

In the ‘news that you thought you would never read’ category, Dubai World (yes, the ‘original’ debt story that started the ‘you-know-what’ crisis that culminated in June of this year) announced that it has successfully won over its creditors to agree to a near $25 billion debt restructuring plan. The ‘victory’ places DW on ‘a sound and stable financial footing.’ So, some pigs can, indeed, fly.

Meanwhile, on the other all-important-and-under-constant-scrutiny front, China, the mixed bag took the following shape: a) Chinese imports grew in August, cutting the trade surplus from gargantuan proportions (nearly $29 billion), to mere gigantic ones ($20 billion). On the other hand, the ‘surplus’ of empty buildings sprouting up all over the country also grew. At rates more than alarming.

All of this, despite rosier than rosy ‘reports’ (okay, manufactured news) that heavy machinery such as wheel-loaders were rolling off assembly lines at rates that can only presage wild rates of future economic growth. The Daily Bell chalks that one up to starry-eyed optimism last seen only just prior to the financial meltdown that began in 2007. At least copper –that certain bellwether- followed some logic as it headed for a weekly drop on concern about future demand…from China (and the US as well).

Watch for Mr. Obama’s press conference, Chinese stats over the weekend, and the on-going battle to try to push gold beyond the last magic number dating back to June. One blogger noted that gold did not ‘get the memo’ that a bear turn did in fact start in June, since it has just about revisited that figure this week.

Memo to you: Do not miss the Kitco eConference that starts on Sunday. No overbooked planes to catch, no hotel beds to scour for bedbugs, no need to eat muffins for lunch. You can attend in your shorts, lemonade in one hand, and the mouse in the other. Where and how else would you be able to see/hear Jim Dines, for example, without going through the aforementioned hassles?

Happy Show Attendance!

PS — You can catch this writer’s musings on the gold market’s fundamentals (yes, they still matter) on Monday morning at 10:30 NY time during said mega-event.

Jon Nadler

Senior Analyst

Kitco Metals Inc.

North America

Blog: http://www.kitco.com/ind/index.html#nadler

Original article link: A Central…Matter or Two